August 10, 2022

By Acuity Trading

Possibly the most nail-biting earnings season in a long time is drawing to a close. If analyst commentary kept you on the edge of your seat, you weren’t alone. Yes, there were some quarterly reports that had us clenching our fists and looking for the nearest wall. But, overall, the Q2 earnings season was much better than feared.

Two Sides of the Coin

The Q2 earnings season this year seemed subdued, especially after the excitement of beat and raise releases in 2021. This made investors feel a tad disappointed. Not devastated, rather like a dragon fruit that leaves a bitter aftertaste.

The results weren’t depressing at all. In fact, the percentage of companies topping expectations in Q2 was within the historical range, albeit at the lower end. As of August 5, 433 of S&P 500 companies had reported their Q2 results, with around 69% reporting revenues ahead of expectations and 77% beating earnings estimates. It is true, however, that the extent of the beat was much lower than what we’ve seen in the last five years.

Cumulatively, these companies managed to grow revenues by more than 15% year-on-year and earnings by almost 8%, despite inflationary pressures, the Russia-Ukraine war, supply chain disruptions and other such challenges.

Moreover, the earnings calls managed to quell fears of analysts and investors alike, with most companies reiterating their full-year guidance.

The Coronavirus Effect: Devil & Deep Blue Sea

In 2021, most of the biggest companies flourished, with coronavirus-related uncertainty abating. People felt increasingly confident of getting back to office, eating out and traveling, supporting reopening stocks. For the second quarter that year, Coca Cola reported 42% revenue growth, Restaurant Brands International posted 37% growth in net sales, Airbnb’s EBITDA skyrocketed 227%, Walt Disney reported strong financials, Gap crushed Wall Street expectations and more.

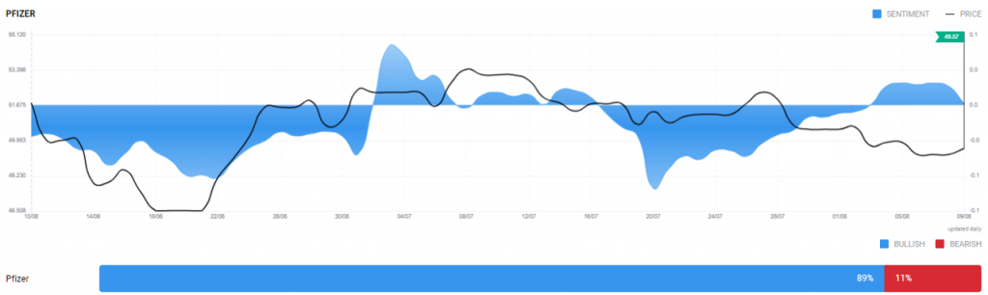

The vaccination drive continued around the world, while people returned to elective treatment as well. This supported pharma stocks. Pharma giant Pfizer reported 98% revenue growth. Logistics companies supporting the vaccination drive also benefited.

This year, the story reversed. On the one hand, pent-up demand had mostly been satisfied. The spread of covid-19 in China and the country’s zero infections policy resulted in lockdowns, aggravating global supply chain issues. On the other hand, people had received their third and even fourth jabs. The demand for vaccinations fell, hurting pharma and related logistics companies.

These are, however, transient factors, which will get equalised as we progress into the back half of the year. Investors seem to understand this and the sentiment for large pharm stocks remains overly positive, as reflected by Acuity’s Sentiment Widget.

Not Go Broke Trying to Look Rich

If there’s one unique theme to the Q2 results this year, it’s that of capital conservation. Many leading names pared back share buybacks in the second quarter. In January, Goldman Sachs projected 2022 to be a record-breaking year for share repurchases. After Q2, we’re nowhere close to Goldman Sachs’s projected $1 trillion in share buybacks. Less than 60% companies reported buybacks in the second quarter, with the amount contracting 12.9% since the first, according to analyst Howard Silverblatt from S&P Dow Jones Indices.

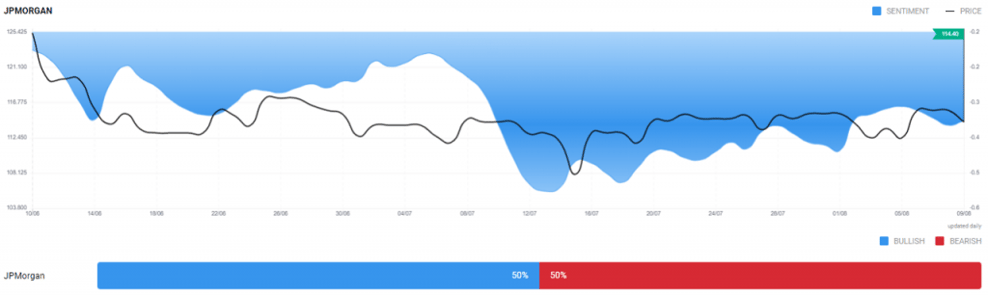

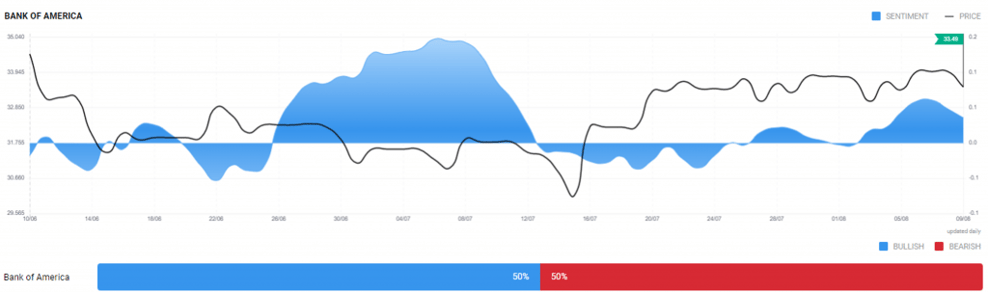

Some non-financial companies like Starbucks and banking majors like JPMorgan, Citigroup and Bank of America halted their share repurchases.

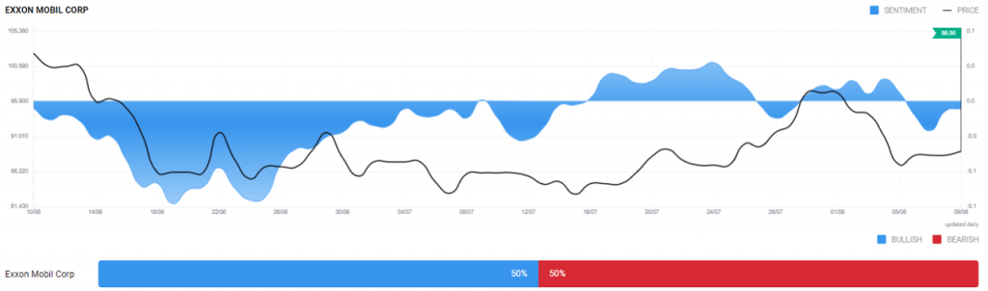

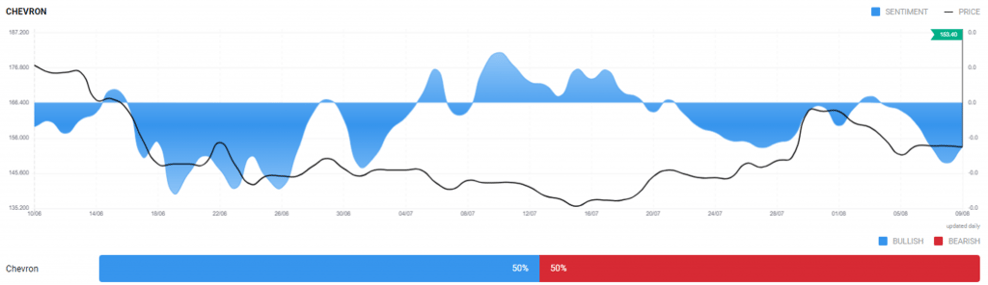

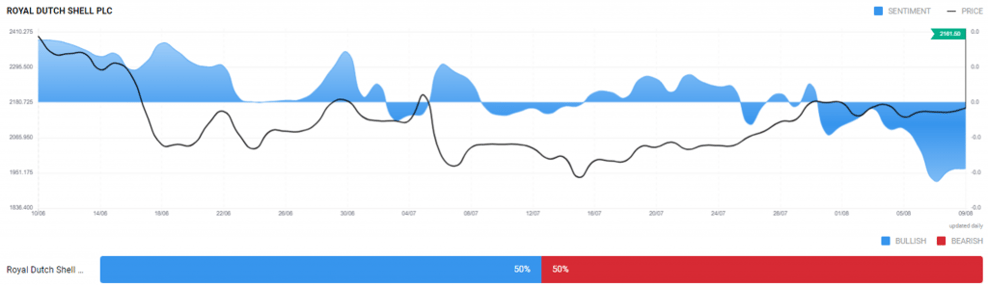

Others decided to conserve capital by suspending or reducing dividends. Less than 3,500 companies declared dividends in July 2022, representing a steep decline from over 5,000 in the same month last year. The only exceptions were tech majors like Apple and energy behemoths. In fact, the world’s biggest oil companies, including ExxonMobil, Chevon, Shell and TotalEnergies, increased their plans to return cash to shareholders via both share repurchases and dividend hikes due to surging oil prices.

Unlike their US peers, European non-financial firms had followed a conservative approach during the worst of the pandemic, helping them maintain higher liquidity on their balance sheets. However, they also refrained from returning cash to shareholders in the second quarter, to brace the challenges that may lie ahead.

Although investors responded the decline in returns by shedding stocks, the strategy to converse capital will play a key role in insulating these companies from possible global economic slowdown ahead.

In fact, companies also held back investments to maintain balance sheet liquidity, bracing for macroeconomic challenges in the back half of the year. For US non-banking companies, cash as a percentage of total assets rose to 7% in Q2 of 2022, from 4% in 2019, while for European non-financials, the ratio rose to 11%, from 9% pre-pandemic.

Looking Ahead

There’s reason to be optimistic for the back half of the year and into 2023. Although company guidance and average analyst estimates for the third quarter have been revised lower, it simply means that expectations are in check. There’s more conservatism now, giving companies some leeway to beat expectations in the upcoming quarters. Investors can also take solace from the fact that most executives sounded confident in their guidance and commentaries during the Q2 earnings calls.