May 5, 2022

By Acuity Trading

The covid-19 pandemic triggered several unprecedented events in the financial markets. We saw negative oil prices, US circuit breakers kicking in three times in the span of a week, and gold prices hitting a record high of $ 2074.88. The yellow metal’s move to a historic high, with investors’ flight to safety, was not surprising.

Post this peak, gold prices subsided, with investor risk appetite being supported by rapid reopening of economies and an impressive global vaccine rollout. Although investors moved to higher-yielding assets, gold didn’t go off their radar.

The Backdrop is Perfect for a Gold Rally

Fast forward to 2022. Economic growth is once again uncertain. The Russia-Ukraine war has worsened the supply crunch, feeding into the commodity supercycle predicted by analysts as the pandemic waned. The resultant impact on overall inflation is posing massive challenges for policymakers worldwide. Even Japan, which has struggled with deflation since the 1990s, has seen a return to inflation. US inflation accelerated to 8.5% in March, the highest since the Great Inflation of the 1980s. The Euro Area recorded an annual inflation rate of 7.5% in March, making it the fifth consecutive month of hitting new records.

Gold has returned to the limelight. After all, it’s the perfect asset – a safe haven (amid the war) and a traditional inflation hedge. Spot prices reached $1,937. However, a combination of factors means that the yellow metal is unlikely to shine as brightly as it did in 2020.

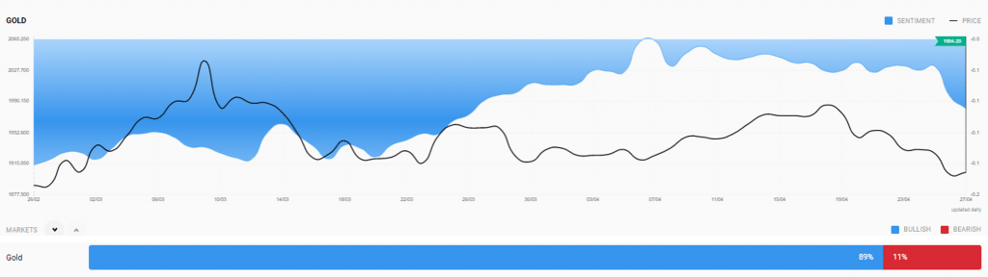

Although the sentiment for the yellow metal is positive, the curve is on a downward trajectory, despite the continued geopolitical and economic concerns, as can be seen on Acuity’s Sentiment Widget.

Why Gold May Not Breach $2,000 Anytime Soon

Inflation

With worsening supply chain constraints and economic activity recovering only moderately, the focus of the major central banks (Fed, ECB, BoE) has shifted to inflation. Let’s take the US as an example. After maintaining a dovish tone for the better part of two years, the Federal Reserve has turned strongly hawkish. The May meeting could see policymakers hike the benchmark interest rate by as much as 0.5% and approve plans to shrink their oversized asset portfolio.

The market’s heightening expectations of Fed rate hikes has pushed the 10-year US treasury rate from 1.56% in January to the current 2.76%. Rising yields increases the opportunity cost of holding non-interest yielding assets, like gold. Such sentiments could continue to dampen gold prices. Despite the IMF lowering its projections for global economic growth and the resurgence of infections in China, analysts maintain their yield estimates around 3%. The 3% nominal yield level for the 10-year US treasury has historically formed a resistance level, most recently seen in 2018.

The Fed now aims to snip these heightened inflation expectations in the bud and to frontend their rate hikes. This limits the potential of any gold rally in the near term. However, it’s important to bear in mind that the Fed can’t raise rates too fast, as this has serious consequences for the labour market. The weakening in gold will likely be proportionate to how quickly the Fed tightens its monetary policy.

Slowdown in Economic Growth

After a year of pandemic-led restrictions, investors were looking forward to a strong economic recovery. Markets took various challenges, like the semiconductor shortage, supply chain issues and labour market disruptions, in their stride. However, they couldn’t ignore the prolonged Russia-Ukraine war.

Experts have lowered their estimates for global economic growth. US GDP growth is projected to decelerate to 3% in 2022. This means central banks will need to spread out their interest rate hikes through the year, while simultaneously addressing supply-side pressures. This spells continued weakness in gold.

The Dual Impact of the Greenback

Gold is not the only safe-haven option. The US dollar is a very popular safe-haven asset for traders and investors alike. With the Fed expected to hike interest rates, market participants may gravitate to the US dollar in the face of geopolitical turmoil or economic concerns.

On the other hand, gold prices are expressed in US dollars in the global markets (XAU/USD). This means any spike in the greenback makes gold more expensive for investors and traders from other countries.

The US dollar index (DXY) has gained 6.21% year to date. The DXY has steadily appreciated due to capital flowing out of emerging markets. The situation was heightened by Russia moving to the perceived safety of USD denominated securities. The DXY is also being boosted by monetary tightening tailwinds. On April 26, the US dollar hit a 2-year high on expectations of the Fed’s balance sheet trimming and a slowdown in China’s growth due to covid restrictions.

The US dollar is also buoyed by the uneven rise in rates between the US and its leading trading partner, EU. While the Fed is incredibly hawkish, the ECB had refrained from taking the same stance. As per ECB President Christine Lagarde, as much as half the inflationary pressures stem from rising energy costs due to the Ukraine war. However, much of the energy demand is for non-discretionary purposes, so raising rates will have only a minimal impact on demand and, therefore, on energy prices and inflation.

The difference in stance of the Fed and ECB will continue to support the US dollar. The euro has already depreciated by 5.7% against the greenback so far in 2022. Such price

uptrends for the greenback may continue in the near term, posing a headwind for gold through most of 2022.

Once the Russia-Ukraine situation eases and global economic growth begins to accelerate, higher risk appetite may further limit gold’s prospects.