June 13, 2022

By Acuity Trading

Retailers spent most of the past two years trying to parry the blows to their business from pandemic restrictions and sparse economic activity.

Governments and central banks supported them with attempts to reignite demand by announcing record fiscal and quantitative easing. In many ways, this was successful, with global growth bouncing back to 6.1% in 2021. However, the bounce back from covid-19 has caused a new foe for retailers and policymakers.

US inflation (CPI) hit 8.5% in March before easing slightly to 8.2% in April. These are levels not seen since the Great Inflation of 1965-82. In April, the UK posted 9% inflation, the highest rate since records began in 1989. The Eurozone economy is also under pressure, with inflation accelerating to 8.1%.

These economies, which were once struggling to sustain price growth, now finds themselves combatting inflation. With inflation hitting consumer disposable income and corporate profits, have stocks become un-investable? Let’s have a look.

The Big Selloff

Several US retail giants, including Walmart, Target and Best Buy, posted their worst quarterly earnings miss in around five years. These missed expectations stroked the already elevated inflation fears. Shares of leading retailers plummeted in response, with many of them attributed their dwindling margins to higher expenses due to supply chain disruptions and changing customer behaviour. So, how worried should we be?

While there are several reports on supply chain shortages, we need to keep in mind that there are three factors contributing to this. Firstly, many parts of the supply chain had downsized during the covid-19 era, with ships being scrapped, factories being closed, and mines being shut down. These will take some time to ramp up, but they will, as some of the biggest global players are investing in this space. Secondly, we witnessed a faster-than-anticipated recovery in demand in the advanced economies, especially the US. Although the steep rise in demand worsens the situation in the near term, it is good news for the longer term.

Commodity supply has also suffered from the Russian invasion of Ukraine. Over the past two years, the Bloomberg Commodity Index has doubled. Oil, another key input cost for most retailers, has increased more than 60% year to date. These are likely to reach a peak soon and begin to cool. The China covid scenario has already begun to ease.

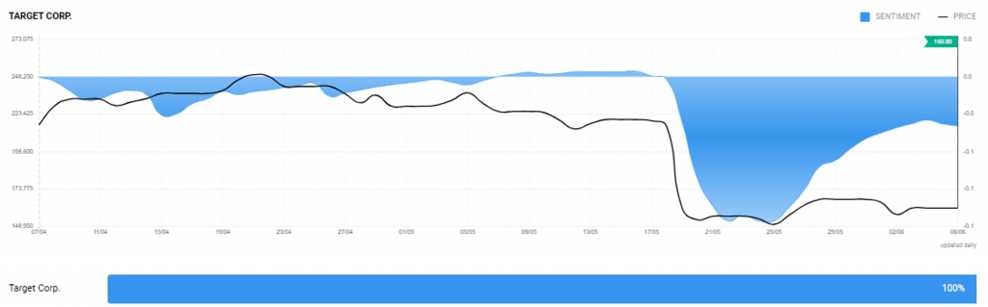

On the other hand, the big sell off in retail stocks presents opportunities. Walmart is down almost 14% and Costco 16% year to date. Market sentiment for Target, which has lost more than 30% this year, has turned positive, as can be seen on Acuity’s Sentiment Widget.

Investors are beginning to realise that these are behemoths in their industry, with the wherewithal to survive the current challenges.

On the other hand, Macy’s and Dollar Tree have posted solid earnings. Foot Locker and Lululemon managed to beat earnings expectations. Foot Locker benefited because its business is focused on the US market and Lululemon because it caters to the luxury segment which is not price sensitive.

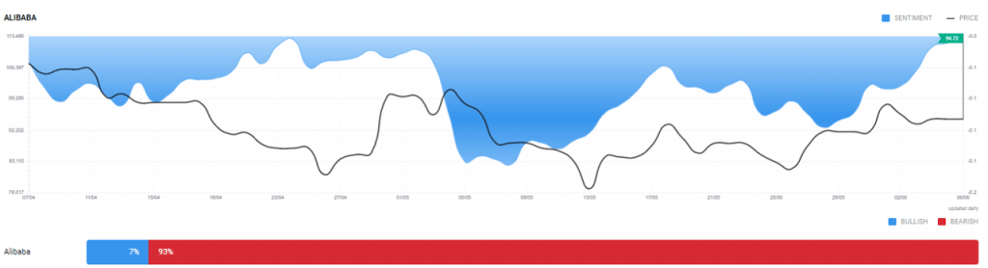

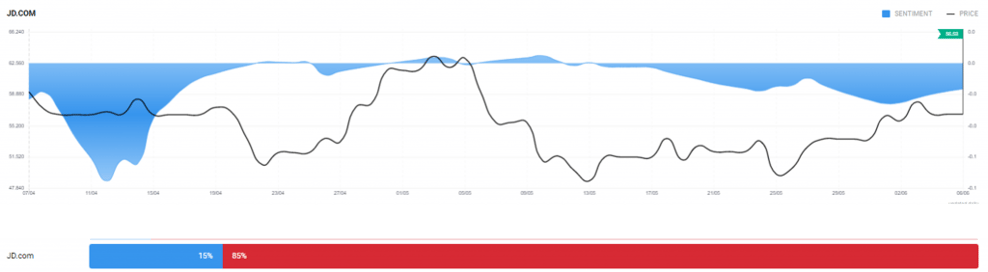

Chinese ecommerce giants, Alibaba, JD.com and Pinduoduo reported sales growth and higher-than-expected earnings for the first quarter. However, the sentiment for Chinese stocks continues to be negative, as per Acuity’s Sentiment Widget.

While inflation is at record highs, the situation could get worsen. Faced with higher expenses, companies are trying to pass on the burden by increasing the price of their offerings, sparking more inflation.

Inflation has occupied centre stage in the financial media and consumers go into purchases expecting higher prices.

The Role of Central Banks

Price stability is the core focus for central banks. They influence the economy’s aggregate demand by increasing or decreasing money supply, which in turn affects prices. Central banks do this by changing interest rates. A higher interest rate lowers money supply, which curbs demand. A lower interest rate lowers the cost of money, allowing the economy more access to funds to increase consumption and investment, which increases the prices of the goods consumed.

In advanced economies, especially in the US, the focus has been on raising interest rates. The Fed has already increased its benchmark rate from 0.25% at the beginning of the year to 1% in May. However, central banks need to realise that inflation control must be balanced with growth. With supply-side led inflation, due to supply chain disruptions and geopolitical conflicts, hiking rates might not actually work.

Central banks need to monitor supply side cues. They need to pause their tightening activity to reassess the state of the economy.

More news

Moody’s Has ‘Negative’ Rating for China. Why is Its Economy in Trouble?

Moody’s has reaffirmed its “negative” outlook on China’s sovereign credit rating. The credit ratings firm had lowered China’s rating from “stable” to...

Is Xi Jinping Shifting his Stance Towards Chinese Tech Companies?

On February 17, 2025, China’s President Xi Jinping called a meeting of prominent tech leaders in the country, including Alibaba’s co-founder, Jack...