Commodities

August 20, 2021

By Acuity Trading

We’re well into the back half of the year and oil prices remain below $100 per barrel. This seems like such an achievement, given that oil prices unprecedentedly hit negative territory in April last year. With demand hitting rock bottom, producers had no storage available and agreed to actually pay spot buyers to take crude. Following those dark days for the oil market, demand has significantly recovered. While spot prices traded at historical discounts to futures prices in 2020, the situation has flipped. The world’s economy needs oil again and needs it now.

Oil’s previous supercycle lasted for a decade, between 2004 and 2014, when a China-led commodity market boom pushed oil to over $100 per barrel. So, are we headed into an oil supercycle? Will suppliers again be struggling to keep up with soaring demand? Most importantly, will oil breach the key $100 market and spike to $200?

Drawing on Reserves: A Consumption Recovery Story

Demand is what fuels a supercycle. In the 2004-2014 period, Chinese industrialisation drove growth. In 2021, the narrative has changed to countries across the globe emerging from economic contraction – a butterfly shaking off the remnants of its cocoon, to soar. The small roadblock to this narrative is that the cocoon, aka covid-19, seems difficult to shaken off. On the contrary, the virus keeps coming back in mutated forms to pose new challenges and slowing down economic growth.

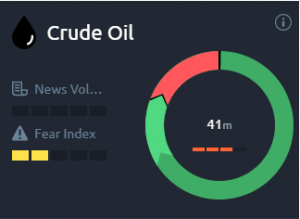

Although the Delta variant poses meaningful threat to the promising growth stories in Asia, including China, India, Korea, and Japan, the optimistic narrative holds. In July, the IMF released projections for global growth at 6% for 2021 and 4.9% for 2022, despite stuttering growth in key Asian countries. Drawdowns in oil inventories persisted throughout the first half of 2021 and, while the pace is expected to decelerate in the second half, experts expect the demand for oil to continue rising, supported by the current pace of vaccine rollouts and massive stimulus packages in advanced economies. Against this backdrop, the sentiment for oil remains positive, as can be seen in the Acuity Trading Dashboard.

.png?width=252&height=294&name=1%20(1).png)

Fill Her Up: A Case for Supply Shortages

OPEC+ and the US voluntarily cut oil supply through 2020. Some supply has returned since, but OPEC+ is unlikely to completely phase out production cuts before September 2022. While the EIA expects global production to outpace demand by 2022, this is highly unlikely.

For one, there has been no new investment in production since 2014. Also, the uncertainty over demand can prolong supply under-investment.

All That Talk About Going Green

How much will rising environmental consciousness impact prices? The pandemic seems to have brought Going Green into everyone’s radar. The transition to green technologies is among the greatest threats to oil, as governments seem determined to phase out fossil fuel vehicles. The Biden administration has proposed a $174 billion investment in the EV market.

In the near term, however, this trend towards green could actually benefit oil. Even as EVs gain popularity, setting up their manufacturing facilities and charging stations will rely on existing oil-powered infrastructure, for everything from fabrication to logistics. Growth in EVs will, therefore, likely be a tailwind for oil prices in the short run. The ramping up of the EV market is driving a rally in the overall commodity market, including in metals like silver and palladium. The overly positive sentiment for these metals can be seen on the Acuity Trading Dashboard.

.png?width=284&height=202&name=2%20(1).png)

Much like the previous decade, China is determined to shape global economic growth in the years ahead. Much of its recovery strategy does not encompass green initiatives. And those that do, are being achieved on the back of its existing oil and coal-powered economy, increasing oil demand. Moreover, as China grows, so will its energy demand. So, even if the mix shifts, the absolute consumption of oil may remain the same or even grow in the near term.

The trend of green investing has led investors to shun oil stocks in favour of ESG assets. In 2020, ESG indices outperform their conventional counterparts. Similar trends can be seen in the Fixed Income space, with the green bond market surpassing $1 trillion in 2020. The impact on oil companies is twofold. First, it impacts their access to funding, threatening their ability to turn on supply, conduct explorations and invest in new projects. Secondly, many oil majors are state-owned and were forced to maintain a high dividend or share buyback policy even during the pandemic, reducing the cash flow available for reinvestment. Both these factors pose curtail their ability to ramp up supply.

Even in an accelerated green energy transition scenario, McKinsey estimates 23 million barrels of new production will be required to meet demand after 2030.

How likely are oil prices to hit $200 per barrel? Much depends on how quickly economies recover from the pandemic and how rapidly they transition to a green economy. The transition is likely to be stickier than policymakers expect, leading to a continued rise in oil consumption at east over the next couple of years.

More news

Is Xi Jinping Shifting his Stance Towards Chinese Tech Companies?

On February 17, 2025, China’s President Xi Jinping called a meeting of prominent tech leaders in the country, including Alibaba’s co-founder, Jack...

Australia’s Economy Continues Declining. Is Low Tech Adoption to Blame?

Australia, once called the "economic poster child," has now been termed a "problem child” by McKinsey. The nation had witnessed 33 consecutive years...