September 20, 2023

By Acuity Trading

Faced with decades-high inflation, the Federal Reserve has driven its benchmark rate to a range of 5.25% to 5.5%, the highest since 2001. Is the Fed done or simply taking a breather? The last hike, of 25 basis points, was announced in July and policymakers have kept rates unchanged since. Markets have widely penciled in one more rate increase this year and look forward to cuts next year, with projections hovering around one percentage point.

The impact of the Fed’s tightening cycle having run its course could have far-reaching effects on the global financial markets. Here’s a deep dive into that.

Impact on the US Economy

The objective of rate hikes is to discourage spending by businesses and consumers, which then cools inflation. But the tightening of credit conditions also cools economic growth, sending shivers down the spine of investors.

While the US seems to have dodged a recession, the impact of previous rate hikes will continue to be felt. The economy appears resilient and poised for a soft landing, with growth slowing to a little below 1% year-on-year over the next few quarters. Unemployment is likely to continue rising, from 3.8% in August to well above 4% by yearend 2024. The good news is that inflation will continue easing and come close to the Fed’s targeted 2% by then.

Stock Markets

The S&P500 has gained almost 17% year to date, the Dow Jones is up 4% and the Nasdaq 100 has added a whopping 41%. Shares of the tech giants, which exited 2022 in a sorry state, have rallied so far this year. Apple and Microsoft are up 40% year to date, while Google-parent Alphabet is 50% higher and Amazon has added almost 60%.

US stock markets seem to have already priced in the pause and enthusiasm around the economy is high. This is reflected in Acuity’s Research Terminal dashboard.

The positive sentiment for top companies is also reflected by Acuity’s AssetIQ widget.

A slowdown in the US economy could be accompanied by some serious profit taking by investors. One segment that looks attractive is energy stocks. Oil prices have been on an uptrend and are hovering around yearly highs. The 25% increase in WTI and Brend crude futures since late June is not fully reflected in energy stock prices.

The US is the world’s largest importer of goods, with over $3 trillion in imports in 2022. Any slowdown in the US economy has a trickle-down impact on its largest trading partners, namely China, EU, Mexico, Canada, Japan, India, and UK. Conversely, elevated interest rates in the US encourage investors to pull money away from emerging markets. A pause in rate hikes could rekindle interest in riskier equity markets, like Brazil, India and South Africa.

Forex Markets

Interest rate hikes supported the US dollar, taking it to two-decade highs in September 2022. Even after gaining more than 12% last year, the greenback has maintained an uptrend, albeit less steep, so far in 2023. While the greenback still has room for appreciation till yearend, it may begin weakening against most major currencies as 2024 progresses.

Inflation has proved stickier in the EU and UK. The European Central Bank and Bank of England are poised to continue their hawkish stance. The ECB hiked rates for the tenth straight month in September, taking its benchmark interest rate to 4%. The BoE seems steadfast in its battle against inflation too.

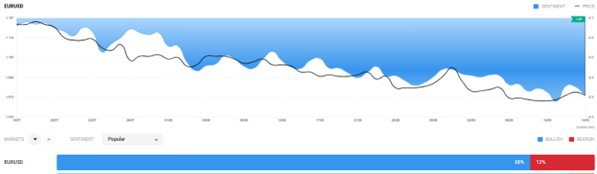

The Fed pausing rate hikes and the ECB and BoE continuing monetary tightening could see investors transferring funds from the US dollar to the euro and pound. Despite the EU’s stagnant growth outlook, the euro could reach parity with the US dollar again before the year ends. This can be seen on Acuity’s Sentiment widget.

Although the GBP/USD has appreciated so far in 2023, it could continue adding to its gains. The JPY/USD, which has declined by more than 10% this year, could recover some of its losses.

As the upward trajectory of the US dollar fades, investors may increasingly turn towards high beta currencies, like the South African rand, Brazilian real and the Turkish lira.

Metals and Commodities

Inflation triggers a rise in all assets. But strength in the US dollar has eroded the shine off metals and commodities. This is because these are quoted in the US dollar and a stronger greenback makes metals and commodities more expensive for foreign currency users, dampening their demand.

As inflation eases, prices of commodities and metals may decline. On the other hand, a weakening US dollar will drive demand and, consequently, the price of commodities and metals.

Currently, the US labour market is cooling gradually, and the economy continues to grow. Against this backdrop, the Fed may announce a rate hike at its November meeting. Even if interest rates have peaked, they are the highest in more than two decades. This means elevated interest rates are here to stay.

More news

Is Xi Jinping Shifting his Stance Towards Chinese Tech Companies?

On February 17, 2025, China’s President Xi Jinping called a meeting of prominent tech leaders in the country, including Alibaba’s co-founder, Jack...

Australia’s Economy Continues Declining. Is Low Tech Adoption to Blame?

Australia, once called the "economic poster child," has now been termed a "problem child” by McKinsey. The nation had witnessed 33 consecutive years...